Last week I shared some fascinating stories (scintillating, really….) about how debt is more of a roadblock than a goal.

What’s that debt roadblock costing you? Tons.

A credit card company wooed me with it’s sweet swan song just after college (in the dark days when I was in debt up to my eyeballs). It must have been the best song ever, because the interest rate was 21%. Throw in a $6,000 limit and we maxed that baby out.

Annual cost to us? $1,260.

I know there are people out there struggling with debt just like I did; people who say, “Well….that’s the cost….what else can I do?”

We need to lower that huge anchor of a fee…even if only by a little. Let me show you what I mean.

Let’s Perform Some Debt Math

Imagine that you found a new credit card at 15% rather than the 21% card you’d previously used. Dream!

New cost per year on this card vs. the old evil 21%’er? $900.

We just saved $360.

Of course, you’re a smart person, and what do smart people do? They apply that $360 to the new 15% card. Over the course of the year you’re throwing that toward principle payments, which lowers your interest costs in year #2 to $846.

Just by changing a credit card we walloped a ton of money toward our debt.

Aren’t we brilliant? Of course we are!

Now we have $954 to save that we didn’t have with the old card. In two years, by just lowering the interest payment from 21% to 15%, we nearly saved $1,000.

My Story (feel free to add this to my Wikipedia entry)

When I first was accumulating debt, I—like most people around me—was pretty naive about the process (stupid might be a better word). I took on any new debt that I could….AND because I was busy paying down debt with every last penny, when my car chugged its last breath I had to go and beg for another loan.

It never seemed to let up.

I was an equal opportunity borrower, and I didn’t care about the interest rate. 25% Fair enough! My strategy? I was a drowning man, and a life preserver made out of saltine crackers was better than no life preserver at all……

There Are Only Two Ways Out of Debt

1) Earn more money and save it. My income began rising quickly. My spouse’s income after college also began to rise. We were able to use this money to pay down tons of debt.

I made this point #1 for a reason. Many people look for ways to cut corners….they’ll spend hours trying to cut an extra $25 off their utility bills. In that same time, they could have easily probably made $50. Sure, saving dough is a great idea, but don’t forget that your ability to earn money can also save the day!

2) Build a cash reserve and slash expenses. I already mentioned why you want to build an emergency fund before paying down your debt here. If you doubt me, that’s fine….but I’ve helped hundred of people work through debt and this is your first time. I’ve never had an experienced “debt getter-outer” fight me on the topic of building an emergency fund first.

In my own experience, I had to have that fund to bridge the “bad times” when stuff would happen. The furnace broke down. My car died. My son went to the hospital and we had a monster deductible. If it weren’t for that fund, we would have gone right back into debt.

I’ve tried that approach, too. Here’s what happens: you get discouraged. You say f$%k it….let’s celebrate a little because we’re tired. It doesn’t work.

One way to slash expenses is to cut your interest payments.

Interest Slashing Ideas:

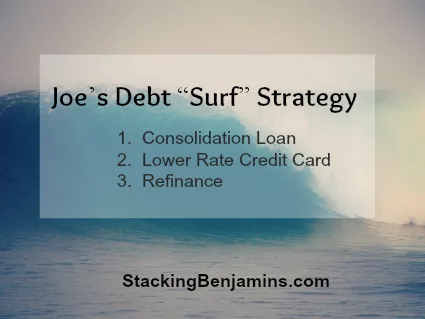

1) Find a consolidation loan. While this interest rate is higher than option #2 below, I like it better because you can divorce your credit card, which was the problem in the first place.

2) “Surf” your interest rate down to a lower rate card. This is a duct tape solution, but it saves you a ton of money. Some people I’ve met haven’t ever heard the term “surfing,” but when I was a financial planner, we used it all the time. We’d surf the giant wave down to a lower rate card. Often that rate was a promotional rate (0% for six months….). When the wave rose (the interest rate jumped up because the promotional period was over), we’d surf down to a new card again.

3) Refinance something. This one can be effective but is horrible. Sure, you’ll get a much lower interest rate on your debt and in many cases it can be tax deductible. But you just turned that hamburger you bought on credit into a 30 year loan. How ugly is that?

Plus…now your house is on the line. If something goes horribly wrong (disability, anyone?), you could now lose your home.

Yuck.

I don’t know why, but generally, I’ve found credit unions are easier to work with than banks on consolidation loans. Also, I generally prefer a mortgage broker to a single bank. I also like dealing with humans rather than finding some bank I’ve never heard of online….but that’s me. I want to look the representative of my lending institution in the eye. While that might not carry the weight it used to, it’s still important to me. Plus, I’m hoping that once I find someone I can trust, I can rely on them in the future. Nothing I hate more than reinventing the wheel every few years……

Lower your interest rates! Pay down your debt! Go forth an conquer!

Photo: xJason.Rogersx

Debt is nasty stuff.. Especially at the higher interest rates.

if you do find yourself in that situation, I wouldn’t hesitate to transfer your balances to a lower rate card when you are trying to pay it off.. Paying the “transfer fee” in the short term well typically be well worth the cost..

Just make sure you cut up your high rate card when you do this!

Good point on raising income, Joe. It gets lost in a lot of the personal finance blogs, but a dollar earned is nearly as good as a dollar saved.

I much prefer real people as well. Somehow they seem to work harder for you if you keep running into them at the grocery store. Of course it goes both ways. I’ve had long discussions with people about glasses or pink eye in the cereal aisle.

When we were paying off our debt, transferring to lower interest rates saved us thousands. I’m not sure why we kept debt at 20% on some of those cards for so long, but live and learn.

I am a big fan of increasing income. I made it a priority throughout my education to make more and I have continued to grow my income.

I used to be an over spender and I was in debt because of it. It truly is awful. I am a better person because of it but I do wish I didn’t have to go through it.