Hey there, Stackers! Joe here, coming to you live from the subterranean glory of my mom’s basement. I’d tell you what Doug is doing right now, but he’s currently trying to see if he can fit an entire sleeve of Thin Mints into his mouth at once. (Spoiler: He’s at four, and things are looking grim for the neighborhood Girl Scout troop’s inventory.)

While Doug works on his dental bills, let’s talk about something that usually makes people’s eyes gloss over faster than a Krispy Kreme donut: Taxes.

Wait! Don’t click away! I promise this isn’t going to be a lecture from your high school economics teacher who smelled like old ham. We’re talking about the Tax Triangle. If you get this right, you’re basically a financial ninja. If you get it wrong, you’re essentially leaving a giant tip for Uncle Sam, and trust me, he doesn’t need the extra cash for his hair plugs.

Plus, 2026 is a massive year for your wallet. If you haven’t checked the calendar lately (or if you’re still using a 1984 Garfield wall calendar like Doug), we are staring down some big changes in the tax code.

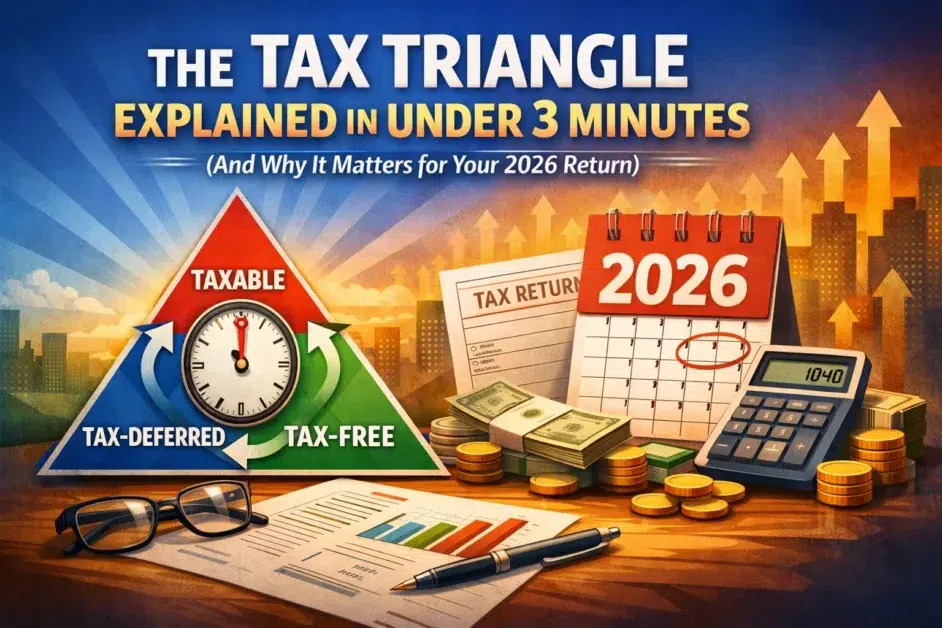

What on Earth is the Tax Triangle?

Imagine a triangle. (I know, high-level math here). Each corner represents a different way the government gets its grubby little paws on your money. Most people spend their whole lives shoving money into just one corner. That’s like trying to sit on a one-legged stool, it’s uncomfortable, and you’re probably going to end up on the floor with a bruised ego.

The Tax Triangle is all about Tax Diversification. You diversify your investments, right? You don’t put all your money into “Doug’s Discount Scuba Gear.” So why would you dput all your money into one type of tax bucket?

Corner #1: The Tax-Deferred “IOU” (The Traditional Route)

This is the corner most people know. It’s your Traditional 401(k), your 403(b), or your Traditional IRA.

The Deal: You put money in today, and the government says, “Hey, cool, don’t pay us taxes on that right now.” You get a tax break today! It feels great. It’s like getting a free appetizer at a restaurant.

The Catch: Uncle Sam is a patient man. He’s sitting in the corner of the restaurant waiting for you to finish your steak. When you take that money out in retirement, he wants his cut. And he wants it at ordinary income rates.

If you have $1 million in a Traditional 401(k), you don’t actually have $1 million. You have maybe $750,000, and the government has a $250,000 lien on your life. If tax rates go up in the future (and spoiler alert: look at the national debt), your “partner” Uncle Sam might decide he wants a bigger piece of your steak.

Corner #2: The Taxable “Pay-As-You-Go” (The Bridge)

This is your standard brokerage account. You went to work, you got paid, you paid taxes on that paycheck, and then you invested the leftovers in stocks, bonds, or maybe some really weird niche ETFs.

The Deal: You’ve already paid income tax on the seed. Now, you only pay taxes on the growth (capital gains) and the dividends.

The Catch: You pay taxes every year. If your mutual fund spits out a dividend, you owe. If you sell a stock for a profit to buy a jet ski, you owe.

The Perk: This is your “flexibility” money. There are no “59 ½” rules here. If you want to retire at 45 and live on a boat, this is the money that gets you there. It’s the bridge between your working years and your “yelling at kids to get off my lawn” years.

Corner #3: The Tax-Free “Holy Grail” (The Roth)

This is the corner where the angels sing. We’re talking Roth IRAs, Roth 401(k)s, and even Health Savings Accounts (HSAs) if you use them right.

The Deal: You pay taxes on the money before it goes in. You get no tax break today. It’s like paying for your meal before you even sit down.

The Perk: Once that money is in the account, it grows tax-free. When you take it out in retirement? Zero taxes. If you turn $50,000 into $500,000, you keep all five hundred grand. Uncle Sam gets zip. Nada. Bupkis.

Why This Matters for Your 2026 Return (The “Oh Crap” Moment)

“But Joe,” you say, “2026 is forever away! I haven’t even decided what I’m having for lunch today!”

Here’s the deal: The Tax Cuts and Jobs Act (TCJA) of 2017, the thing that lowered almost everyone’s tax brackets, is scheduled to sunset at the end of 2025.

Unless Congress acts (and when do they ever act on time?), tax rates are going back up on January 1, 2026. Your 12% bracket might jump to 15%. Your 22% might jump to 25%.

If you are 100% heavy in the Tax-Deferred corner, you are about to see your future tax bill get a lot more expensive. This is why we’re talking about this now. You have a window of time to move money around, maybe do some Roth conversions, or change your 401(k) contributions to the Roth side while the “sale” on taxes is still on.

As our friend Robert Farrington discussed when we looked at the best tax software for 2026, being prepared for these shifts is the difference between a comfortable retirement and one where you’re eating generic-brand cat food. (No offense to the cats.)

The “Perfect” Triangle: How Much Should You Have?

OG (our resident cranky financial expert) usually says there’s no “perfect” number because everyone’s life is a different flavor of chaos. But a good rule of thumb for a balanced Tax Triangle looks like this:

- Tax-Deferred: 40% (Your employer match, your old 401(k)s)

- Tax-Free: 30% (Your Roth accounts, your “I’m never paying taxes again” stash)

- Taxable: 30% (Your “I might want to buy a cabin/retire early” fund)

If you’re sitting there realizing you have 95% in a Traditional 401(k) and 5% in a checking account, don’t panic. You’re not alone. Most people start late. In fact, we’ve got a whole guide on how to make a million after starting late.

Strategies to Balance Your Triangle

So, how do you actually move the needle?

- The Roth Conversion: If you think taxes are going up in 2026, you might want to move some money from your Traditional IRA to a Roth IRA now. You’ll pay taxes today at the lower rates to avoid paying higher rates later. It’s like buying your winter coat in July when it’s 90 degrees out, it feels weird, but you’ll be glad you did it when the blizzard hits.

- The HSA Triple Threat: If you have a high-deductible health plan, the HSA is the only account that is triple-tax-advantaged. It’s tax-deductible going in, grows tax-free, and is tax-free coming out for medical expenses. It’s basically the “cheat code” of the Tax Triangle.

- Check Your Contributions: Next time you log into your work portal to change your password for the 14th time this month, check if they offer a Roth 401(k). Many people just default to the Traditional. Switching your future contributions to Roth can help balance that triangle without you even feeling it.

Avoid the “Cliffs”

One thing people forget is that your “taxable income” in retirement affects more than just your tax bill. It affects your Medicare premiums.

Ever heard of IRMAA? It sounds like a character from The Golden Girls, but it’s actually the Income-Related Monthly Adjustment Amount. If you take too much money out of your Tax-Deferred corner, the government says, “Oh, you’re rich! You get to pay more for Medicare!”

By having a healthy Tax-Free corner (the Roth), you can pull money out to live on without it counting toward that “rich person” limit. You stay below the cliff, keep your Medicare costs down, and still have enough money to buy the good brand of coffee.

Final Thoughts from the Basement

Look, I get it. Taxes are about as exciting as watching paint dry on a humid day. But understanding the Tax Triangle isn’t about being a math genius; it’s about flexibility.

Future-You is going to be sitting on a porch somewhere. Future-You doesn’t want to be worried about what Congress is doing with tax brackets. Future-You wants to know that no matter what happens, you have a bucket of money that the IRS can’t touch.

If you’re feeling overwhelmed, don’t sweat it. Just start by looking at where your money is currently sitting. If your triangle looks more like a single dot, it’s time to start branching out.

If you have questions or just want to tell Doug he has a crumb on his chin, reach out to us. We love hearing from Stackers who are taking control of their financial future.

Now, if you’ll excuse me, I have to go help Doug. He’s currently stuck in his “Scuba-Fitness” resistance band and I think he’s losing circulation in his left foot.

Keep stacking those Benjamins!

: Joe

(P.S. If you want to see the full map of everything we’ve ever talked about: including the weird stuff: check out our sitemap. It’s like a treasure map, but with fewer pirates and more index funds.)

Leave a Reply